In active real estate investing, access to capital is often far more important than finding inch-perfect loan terms. Hard money lenders exist to satisfy that basic premise.

By providing short-term, asset-backed financing, they allow investors to move quickly when traditional lenders can’t keep the same aggressive tempo.

The premise is simple: unlike banks, hard money loan lenders underwrite deals based largely on the property and exit strategy, not tax returns or lengthy credit reviews.

Common reasons investors work with hard money lenders include:

- Fast closings: many loans are funded within 5 to 14 days

- Higher LTC ratios: often more flexible than conventional financing

- Asset-based decisions: property value carries more weight than credit history

- Practical use cases: frequently used for fix-and-flips, rental purchases, and construction

The following comparison table and lender reviews will help investors compare options clearly and identify the best hard money lenders for their specific desires.

Top 10 Hard Money Lenders In 2026

Compare Top Hard Money Lenders at a Glance

That’s not to say that all hard money lenders operate the same way, of course. Various nuances can materially affect a deal, such as differences in rates, leverage, or closing speed.

This side-by-side overview highlights how several hard money loan lenders compare on core factors investors typically evaluate first, including pricing ranges, loan structure, and execution speed.

At a glance, this is what you can expect from the lenders on this list:

| Lender | Typical Rates | Loan Terms | LTC / LTV | Closing Speed | Best For |

|---|---|---|---|---|---|

| New Silver | 8.5%–11% | 12–24 months | Up to 90% LTC | As fast as 5 days | Tech-driven investors needing speed |

| LendingOne | 9.5%–12.5% | 12–24 months | Up to 90% LTC | ~7 days | Portfolio and multi-strategy investors |

| Lima One Capital | 9%–13% | 12–24 months | Up to 85% LTC | 10–15 days | Scaled and repeat investors |

| Asset Based Lending (ABL) | 10%–13% | 12–24 months | Up to 80% LTC | 10–14 days | Mixed-use and commercial-adjacent deals |

| We Lend | 9%–12% | Short-term | Up to 90% LTC | 3–7 days | Low-friction, fast funding |

| Do Hard Money | 10%–13% | 5–12 months | Up to 100% LTC* | 7–14 days | New or capital-constrained investors |

| Kiavi | 9.5%–12% | 12–24 months | Up to 90% LTV | ~7–10 days | High-volume fix-and-flip investors |

| BridgeWell Capital | 10%–13% | 12–24 months | Up to 75% ARV | ~10 days | Value-add and commercial projects |

| Rehab Financial Group | 10%–13% | 12–24 months | Up to 70% ARV | 10–14 days | Rehab-heavy and ground-up projects |

| Fund That Flip | 9.99%+ | 12–24 months | Up to 90% LTC | 7–10 days | Short-term residential flips |

Rates and terms vary based on property type, investor experience, market, and credit profile.

Hard Money Lender Reviews

Finding the best hard money lenders usually comes down to simple, practical details rather than advertised rates behind flashy marketing campaigns.

How quickly deals close, how flexible the terms are, and how consistently a lender executes under contract should be the prime focus. All of the lenders below are widely used by real estate investors and differ in their strengths, depending on deal size, timeline, and experience level.

New Silver – Best for Fast, Tech-Driven Closings

| Interest Rates | 8.5%–11% |

| Origination Fee | 1–3 points |

| Loan Amount | $100,000–$5,000,000 |

| LTC | Up to ~95% |

| Terms | up to 18 months |

| Min Credit Score | 650 |

| Closing Speed | As fast as 5 days |

New Silver is a national private lender known for combining hard money lending with a technology-first underwriting process. Rather than relying on slow, manual workflows, the platform is designed to provide investors with fast visibility into pricing, terms, and deal viability early in the process, which can be crucial when competing for time-sensitive properties.

Generally considered among the best hard money lenders, New Silver is particularly well-suited for investors who prioritize execution speed and clarity over prolonged back-and-forth negotiations. The lender places a strong emphasis on property fundamentals and exit strategies, making it a popular choice for fix-and-flip projects, rental acquisitions, and construction deals where timing is critical.

Another differentiator is New Silver’s integrated tooling, including instant term sheets and proof-of-funds letters, which can help investors move more decisively once under contract. For investors comparing the best hard money lenders in 2026, New Silver stands out for its consistency, transparency, and ability to close quickly at scale.

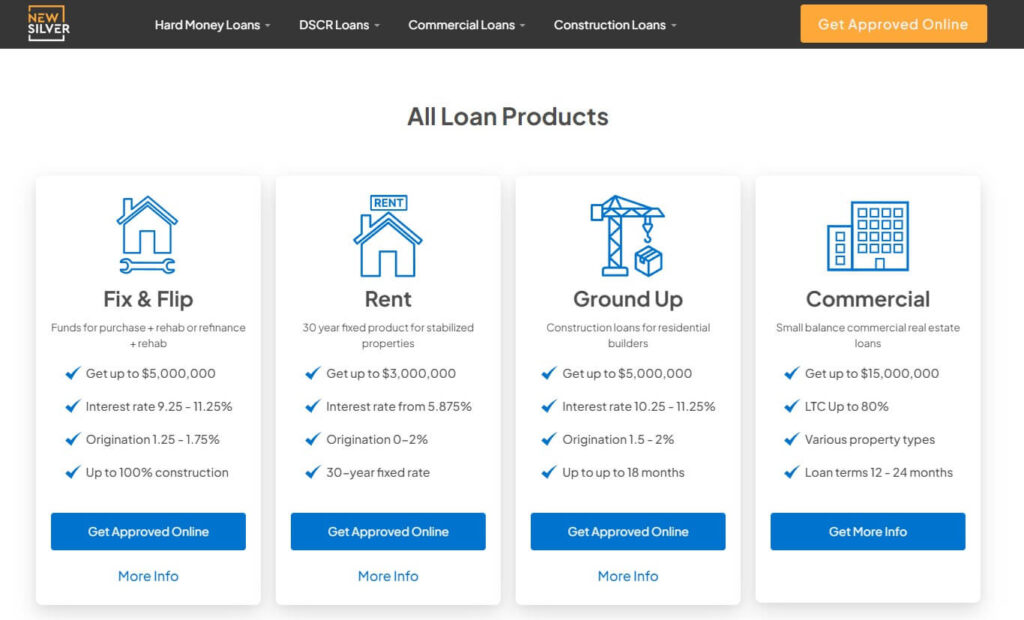

New Silver's Hard Money Loan Products

Fix and flip loans

New Silver’s fix-and-flip hard money loans are short-term loans of 24 months, geared mostly (but not exclusively) towards investors who purchase a property, renovate it, and then resell it.

The interest rates on their hard money loans begin at 8.5%. The minimum loan amount is $100,000 and the maximum that can be borrowed is $5,000,000. New Silver’s renowned speed of closing on fix-and-flip loans (just 5 business days) has helped it earn a reputation as one of the best hard money lenders in the industry.

Rent

DSCR loans offered by the top hard money lenders are designed for investors purchasing property to rent. These loans are 30-year fixed-rate mortgages with amortized payments.

As you might expect, interest rates tend to vary by deal, with qualification based on a combination of property performance, credit profile, and investor experience at the center of it all. Rates start from 6%, the minimum loan amount is $150,000, and the maximum is $3,000,000.

Ground Up

The ground-up construction loan product offered by New Silver is ideal for residential builders. It is a 18-month loan that offers up to 100% financing for construction and up to 90% Loan-To-Cost (LTC). The interest rates on these loans start at 9.75%, and a minimum credit score of 650 is required.

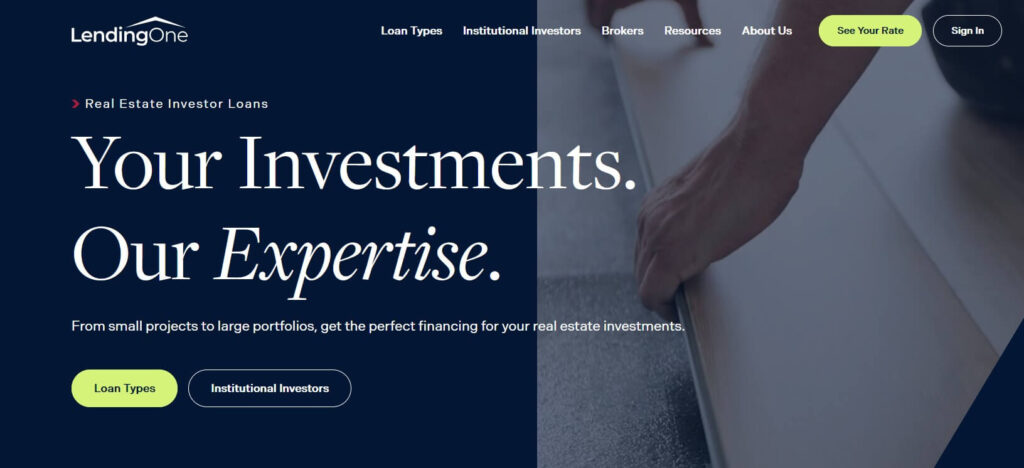

LendingOne – Best for Portfolio and Multi-Strategy Investors

| Interest Rates | ~9.5%–12.5% |

| Origination Fee | ~1.5–2.5 points |

| Loan Amount | Varies |

| LTC / LTV | Up to ~90% LTC |

| Terms | 12–24 months |

| Min Credit Score | Typically mid-600s |

| Closing Speed | ~7 days |

LendingOne is a direct private lender that works with investors across a range of strategies, including fix-and-flip, rental, and transitional deals. The platform is commonly used by borrowers managing multiple properties or combining short-term and longer-term financing within the same portfolio.

Rather than focusing on a single loan type, LendingOne offers flexibility for investors who want continuity as projects evolve, such as moving from a renovation phase into a rental hold. Underwriting places strong emphasis on property fundamentals while still accommodating different experience levels and deal structures.

For investors comparing hard money loan lenders that can support portfolio growth and repeat transactions, LendingOne is often considered for its breadth of programs and consistent execution across deal types.

Lima One Capital – Best for Scaled and Repeat Investors

| Interest Rates | ~9%–13% |

| Origination Fee | ~1–3 points |

| Loan Amount | $100K–$3M |

| LTC / LTV | Up to ~85% LTC |

| Terms | 12–24 months |

| Min Credit Score | Typically mid-600s |

| Closing Speed | ~10–15 days |

Lima One Capital is a national private lender that caters primarily to experienced investors running repeat or higher-volume deals. The platform offers a broad mix of short-term financing options and tends to work best for borrowers who already understand how to structure projects and manage timelines.

Among the various hard money lenders, Lima One is often chosen by investors who need flexibility across different deal types rather than a single, narrowly defined loan product. Its offerings span fix-and-flip, rental, and construction scenarios, making it a practical fit for investors operating at scale or managing multiple projects at once.

For those comparing the best hard money lenders for portfolio growth or repeat transactions, Lima One’s depth of products and consistent execution are probably the main draw.

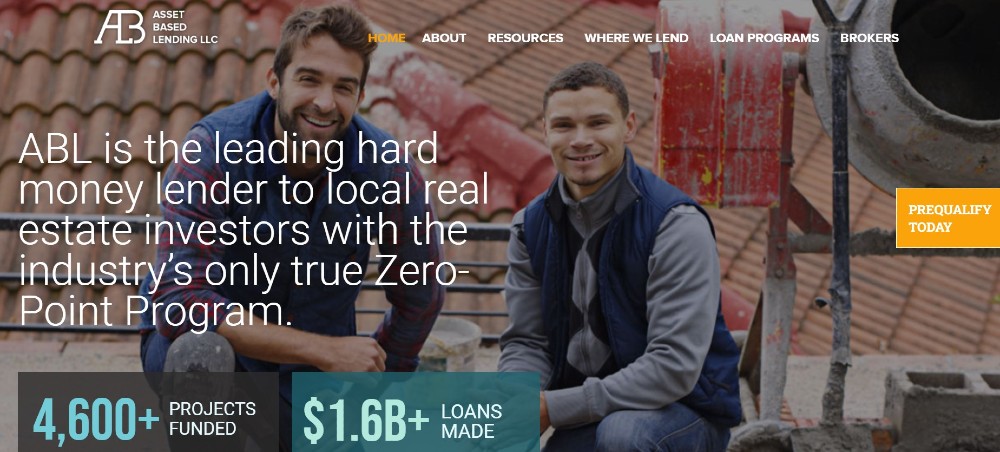

Asset Based Lending (ABL) – Best for Mixed-Use and Commercial-Adjacent Deals

| Interest Rates | ~10%–13% |

| Origination Fee | ~1–3 points |

| Loan Amount | Up to ~$3.5M |

| LTC / LTV | Up to ~80% |

| Terms | 12–24 months |

| Min Credit Score | Typically mid-600s |

| Closing Speed | ~10–14 days |

Asset Based Lending (commonly referred to as ABL) focuses on asset-backed financing for investors working across residential, mixed-use, and light commercial projects. The lender operates in multiple states and is often used by borrowers who need flexibility beyond standard single-family fix-and-flip scenarios.

ABL tends to appeal to investors dealing with properties that don’t fit neatly into conventional categories, such as mixed-use buildings or smaller commercial assets. The underwriting process places strong emphasis on the collateral and project structure, with experience and deal fundamentals carrying more weight than rigid borrower profiles.

For investors comparing the best hard money lenders for projects that fall outside straightforward residential flips, ABL is often considered for its willingness to finance more complex property types.

We Lend – Best for Low-Friction, Fast Funding

| Interest Rates | ~9%–12% |

| Origination Fee | Typically none |

| Loan Amount | Varies |

| LTC / LTV | Up to ~90% |

| Terms | Short-term |

| Min Credit Score | Flexible |

| Closing Speed | ~3–7 days |

We Lend positions itself around simplicity and speed, removing much of the documentation and upfront friction that can slow down deals. The lender is often used when timelines are tight, and investors want fewer conditions standing between approval and funding.

This approach tends to suit fix-and-flip projects and short-term renovations where certainty of execution matters more than custom structuring. Rather than offering a wide menu of specialized products, We Lend focuses on moving straightforward deals quickly and predictably.

For investors comparing hard money lenders with an emphasis on rapid closings and minimal paperwork, We Lend is commonly considered when speed is the primary constraint.

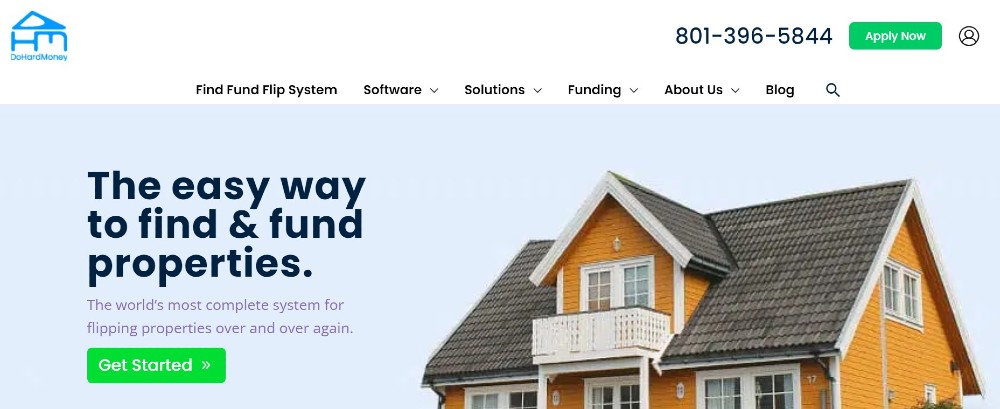

Do Hard Money – Best for New and Capital-Constrained Investors

| Interest Rates | ~10%–13% |

| Origination Fee | Varies |

| Loan Amount | From ~$70K |

| LTC / LTV | Up to ~100% on qualifying deals |

| Terms | 5–12 months |

| Min Credit Score | Typically mid-600s |

| Closing Speed | ~7–14 days |

Do Hard Money is frequently used by investors who are early in their investing journey or working with limited upfront capital. The lender is known for its flexible structures, which can accommodate lower experience levels, particularly in smaller fix-and-flip projects where conventional options may be limited.

Its programs are commonly applied to flips, BRRR strategies, and wholesaling scenarios, with underwriting that places heavier emphasis on the deal itself rather than long borrower histories. This can make Do Hard Money a practical option when access to capital is the primary hurdle.

For investors weighing different hard money lenders and prioritizing flexibility over a polished process, Do Hard Money is often considered when the deal requires creativity more than speed.

Kiavi – Best for High-Volume Fix-and-Flip Investors

| Interest Rates | ~9.5%–12% |

| Origination Fee | ~0.5–2 points |

| Loan Amount | $100K–$1.5M |

| LTC / LTV | Up to ~90% LTV |

| Terms | 12–24 months |

| Min Credit Score | Typically mid-600s |

| Closing Speed | ~7–10 days |

Kiavi is a nationally active lender built for investors running repeat fix-and-flip projects at scale. The platform emphasizes consistency and throughput – two key qualities that appeal to borrowers who value predictable execution over bespoke structuring.

Compared with many hard money loan lenders, Kiavi focuses on standardized underwriting and clearly defined parameters, allowing experienced investors to move quickly once a deal fits within guidelines. This model works particularly well for high-volume flippers who want fewer surprises from deal to deal.

For investors assessing the best hard money lenders for repeat residential flips, Kiavi is often preferred when speed, clarity, and process reliability matter more than maximum flexibility.

BridgeWell Capital – Best for Value-Add and Commercial Projects

| Interest Rates | ~10%–13% |

| Origination Fee | ~1–3 points |

| Loan Amount | $150K–$2M |

| LTC / LTV | Up to ~75% ARV |

| Terms | 12–24 months |

| Min Credit Score | Typically mid-600s |

| Closing Speed | ~10 days |

BridgeWell Capital is often used by investors working on value-add projects that might fall outside ‘straightforward’ residential flips. The lender has been active for many years and tends to work with borrowers who have a clear, forward-thinking plan for stabilization, repositioning, or longer-term hold strategies.

Rather than chasing volume, BridgeWell focuses on deal structure and collateral quality, which makes it a solid option for investors financing mixed-use, small commercial, or transitional assets. That approach can be appealing when flexibility around project scope matters more than shaving a few days off closing.

For investors comparing top hard money lenders for complex or value-add deals, BridgeWell Capital is typically considered for its experience across commercial-adjacent property types.

Rehab Financial Group – Best for Rehab-Heavy and Ground-Up Projects

| Interest Rates | ~10%–13% |

| Origination Fee | ~1–3 points |

| Loan Amount | $50K–$3M |

| LTC / LTV | Up to ~70% ARV |

| Terms | 12–24 months |

| Min Credit Score | Typically mid-600s |

| Closing Speed | ~10–14 days |

If you have a project where the renovation scope is substantial, or construction is a central part of the deal, Rehab Financial Group might be a good option. The lender offers structures that appeal to investors managing heavier rehabs, tear-downs, or ground-up builds where draw schedules and project oversight are a prime consideration.

Rather than prioritizing speed alone, RFG places emphasis on project feasibility and execution planning, which can suit investors with a clear construction strategy and realistic timelines. To that end, this is a practical option for borrowers whose deals require more than simple cosmetic updates.

For investors evaluating hard money lenders for renovation-intensive projects, Rehab Financial Group is commonly considered for its experience supporting complex rehab and construction scenarios.

Fund That Flip – Best for Short-Term Residential Flips

| Interest Rates | ~9.99%–13% |

| Origination Fee | ~1–3 points |

| Loan Amount | From ~$100K |

| LTC / LTV | Up to ~90% LTC |

| Terms | 12–24 months |

| Min Credit Score | Typically mid-600s |

| Closing Speed | ~7–10 days |

Having built a reputation around financing straightforward fix-and-flip deals where timelines are tight and the exit strategy is clearly defined, Fund That Flip is mostly used by investors focused on short-term residential renovation projects.

Its lending model tends to suit investors who already have some experience in managing rehabs and are comfortable working within set parameters rather than highly customized structures. Funding is typically geared toward purchase and renovation costs, with draw schedules meeting project milestones.

For investors comparing hard money lenders for clean, residential flip projects, Fund That Flip is often considered when the priority is executing a defined plan efficiently rather than financing complex or mixed-use assets.

What Are Hard Money Loans?

Hard money loans are short-term, asset-based loans provided by private lenders or lending companies to real estate investors. Again, rather than relying heavily on personal income, tax returns, or long credit histories, hard money lenders focus mostly on the property itself and the strength of the deal.

In short, hard money loans are a practical, wise option when speed, flexibility, or property condition make traditional bank financing difficult.

Unlike conventional mortgages, these loans are designed for investment scenarios where timing is a key factor. Because underwriting is centred on the asset and exit strategy, approvals tend to move much faster, which is why many investors turn to hard money lenders when competing for deals or working with properties that need renovation.

Key characteristics of hard money loans include:

✔️Asset-based security: loans are secured by property value

✔️Short loan terms: typically six to 24 months

✔️Higher interest rates: commonly in the 8%–12% range

✔️Fast approvals and closings: often days rather than weeks

✔️Flexible qualification criteria: fewer rigid underwriting requirements

Most real estate investors use hard money loans across a wide range of scenarios. Common uses include fix-and-flip projects, rental property acquisitions, bridge financing between transactions, ground-up construction, and purchases of properties that don’t qualify for bank loans due to condition or occupancy issues.

From a process standpoint, hard money loan lenders evaluate the property’s current value and after-repair value (ARV), then structure the loan using loan-to-cost (LTC) or loan-to-value (LTV) ratios.

Payments are often interest-only during the loan term, keeping carrying costs predictable. Most investors exit by selling the property or refinancing into longer-term financing once the project stabilizes.

How to Choose a Hard Money Lender

Choosing between hard money lenders is less about finding the lowest advertised rate and more about understanding how each lender operates in practical terms.

Ultimately, the Terms, speed, and reliability can vary quite widely, so comparing options carefully can make a true, meaningful difference to deal outcomes.

Rates and fees should always be evaluated as a package. While it may be tempting to focus on interest rates alone, try and resist the urge: instead, compare APR to understand the total cost. Ask how many origination points are charged and whether there are additional fees for underwriting, document preparation, or draw management.

Speed and reliability are a prerequisite when timelines are tight. Most hard money loan lenders close within five to 15 days, but remember, consistency is just as important as speed. With that in mind, look for lenders with a track record of closing on time and ask whether instant proof-of-funds letters are available.

Loan structure should be another deciding factor. Higher loan-to-cost ratios can reduce the amount of cash you need upfront. If your project involves major renovations or new construction, confirm whether construction financing and draw schedules are supported. Interest-only payment options can also help manage short-term cash flow.

Experience requirements vary by lender, and while some prefer borrowers with a proven track record, others regularly work with first-time investors. Try matching the lender’s expectations to your experience level – it can improve approval odds.

Geographic coverage should never be assumed. Confirm that the lender operates in your market and understand whether they’re a national platform or regionally focused.

Service and technology also play a firm role. Online applications, deal tracking, and responsive communication can simplify the process.

As a final step (and we may be stating the obvious here) , always get quotes from three to five lenders before committing, compare total costs, and read recent borrower reviews before committing.

Bottom Line

Choosing the right hard money lender doesn’t need to be a complicated endeavor. In reality, your choice boils down to the project type, timeline, and experience level you are dealing with.

Either way, we believe the 10 lenders above represent some of the best hard money lenders available to real estate investors in 2026, with each company offering different strengths depending on how you intend to invest.

If fast decisions, upfront terms, and minimal friction are important to you, New Silver offers a streamlined application process built for active investors.

FAQs

Hard money lenders usually focus on the property and the deal itself rather than the borrower’s income or long credit history. Banks rely heavily on financial documentation and longer underwriting processes, which can slow approvals. Because of this, hard money loans are commonly used when speed, flexibility, or property condition make conventional financing impractical.

Rates vary by lender and deal, but interest rates generally fall between 8% and 12%. In addition to interest, many hard money loan lenders charge origination fees, often expressed as points, usually ranging from one to three percent of the loan amount. Total cost depends on loan size, term length, and how quickly the loan is repaid.

Closing timelines are one of the main reasons investors use hard money lenders. In many cases, funding can happen within five to 15 days, assuming the property valuation and documentation move smoothly. This is significantly faster than traditional loans, which often take 30 to 60 days or longer.

Credit requirements are typically more flexible than bank loans. Many lenders look for scores in the mid-600s, but approval is driven more by property value, equity, and exit strategy. A stronger credit profile can still help secure better pricing or terms.

Start by matching the lender to your project type and experience level. Compare total costs, not just rates, and review closing timelines and past borrower feedback. Getting quotes from several lenders helps clarify which option fits your situation best.