The below is for informational purposes only, it is not tax advice or recommendation. Please contact your licensed tax advisor if you have specific questions.

Jump To:

After you’ve successfully sold a flip for a profit, it’s time for the inevitable that comes with every big transaction: paying taxes. If you have not flipped a house before, you may be wondering, how much tax will you have to pay if you flip a house? The answer is that the taxable amount owed can vary depending on the property type, the investor’s income, and other factors we’ll cover in-depth below. As lucrative as fix and flips can be in terms of profits , the tax associated with these projects can be high unless you know how to minimize them.

This article will teach you everything you need to know about fix and flip taxes – how much you are expected to pay, when these payments are due and the best strategies to help you save. There are also set tax benefits that you can gain the advantage of by flipping houses if you know what they are and how to apply them effectively.

Keep reading to find out exactly how much tax you will be liable for if you flip a house this year and the best way to save:

Tax Basics When Flipping A House

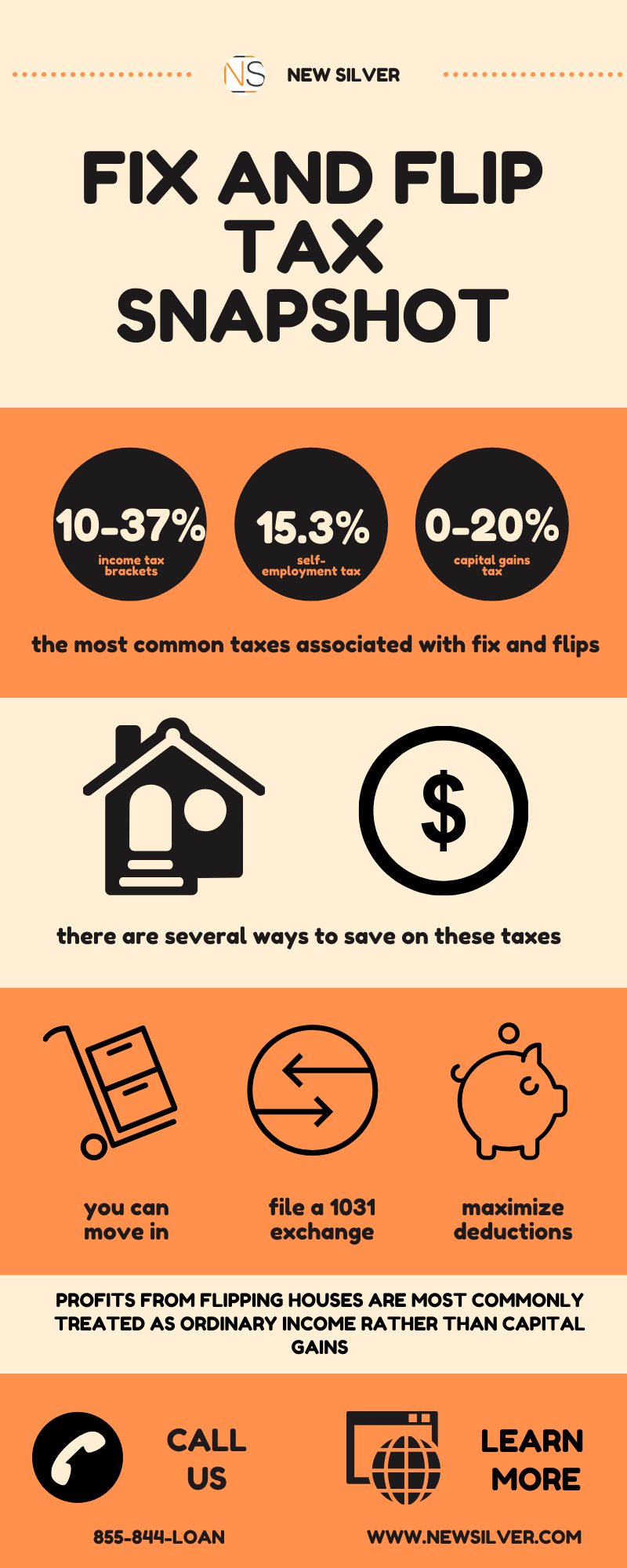

Before you move on to how much will need to be paid, it’s important to understand the basics of how these taxes are structured. Typically, house flipping is not considered to be passive investing by the IRS, and as active income, the investor will need to pay normal income taxes on their net profits within the financial year. These taxes commonly include federal income tax, state income tax, and taxes for self-employment. The majority of fix and flip investors are classified as dealers by the IRS, as the majority of their income comes from flipping properties. This classification in short means that the investor purchases real estate to sell to others over the short-term, and will apply even if the investor only flips properties occasionally.

As a real estate investor, you pay taxes as a business, meaning that gains are taxed as ordinary income no matter the length of the holding period. However, any profits made on properties held longer than a year are subject to capital gains tax going up to 20%. Capital gains taxes apply more to long-term rentals and primary occupation situations, but there are circumstances in which it can apply to flips. If you qualify for capital gains taxes, you can save on self-employment tax which no longer applies. There are short-term capital gains taxes and long-term capital gains taxes , which depend on the time it takes before the property is sold.

You might not necessarily consider your real estate investing to be a business if you do it part-time or have an unrelated, full-time career. According to the IRS though, any real estate investment can be classified as a business whether it is done as part of an agreement or under your own name.

How Much Tax Is Paid On Fix And Flips?

When flipping homes, the total amount of tax you will be liable for will be entirely dependent on both your income tax rate and the federal tax bracket you fall into, while your self-employment taxes will come in at 15.3% up to the amount of $132,900. Tax brackets for 2020 are as follows, with the filing deadline being April 15th, 2021:

- Up to $9,875 is taxed at 10% under normal rates, with no long-term capital gains tax

- Between $9,876 and $40,125 is taxed at 12%, with no long-term capital gains tax

- $40,126 to $85,525 is taxed at 22% and long-term capital gains of 15% apply

- $85,526 to $163,300 is taxed at 24% with long term capital gain tax of 15%

- $163,301 to $207,350 is taxed at 32% with 15% long term capital gain tax

- Between $207,351 and $518,400 is taxed at 35% with long-term capital gains tax of 15%

- Amounts over $520,000 are taxed at 37% with long-term capital gains tax of 20%

These brackets shift somewhat when you are married and filing jointly. If you’re married but don’t want to file with your spouse, your filing status will be “Married filing separately”.

On the other hand, state income taxes are paid based on state income tax brackets. Capital gains tax will also apply, varying depending on the time it took for the property to sell. Under 12 months is considered to be a short term capital gain, which is taxed at the normal income tax rate. Over 12 months leads to classification as a long-term gain where the taxation rate is somewhere between 0% and 20%. This total will also depend on your filing status and total taxable income earned within the financial year.

Ultimately, house flipping taxes can be roughly calculated by multiplying your taxable profit by your ordinary income tax rate. Another calculation method is taking the final sales price of the property, subtracting the total expenses, and available deductions from it. The typical expenses associated with these flips include loan fees and repayments, professional services, materials, and labor to name a few. The profit in these calculations is based on the amount cleared after all expenses have been taken into account.

When Are These Taxes Paid?

Property is classified as inventory, and under this classification, no taxes need to be paid until the final sale of that “inventory” is complete. This means that if you purchase a home in 2019 but don’t sell it until the end of 2020, you only need to pay taxes on the property in 2020.

As a business or self-employed individual, real estate investors do have to prepay their taxes with quarterly estimated tax payments. This applies if you make over $1,000 per year in profits. If you are not generating revenue or income yet, your taxes will need to be filed at the end of the year. You’ll need to file a Schedule C form, also known as a 1040 Profit & Loss Form by the 15th of January, April, June, and September.

Saving On Taxes

There are several ways to reduce taxes on flipping houses. For instance, there are some special situations in which a house flip will not be subject to the usual income taxes.

In terms of self-employment tax, you can register an S-Corp and pay yourself a “reasonable salary”. This would limit your payable amount to 15.3% of the salary amount and the remaining amount would be exempt from this tax. S-Corp owners can additionally choose between receiving a salary or receiving dividends, with dividends taxed at a lower rate than self-employment income. S-Corps also offer another advantage in the form of a 20% deduction for pass-through entities.

There is another tax-saving method available to investors that flip houses. Investors have the option to file a 1031 Exchange, under which you can defer your capital gains tax bill on a property that is sold, as long as a similar property is purchased with the profits from the first property sale.

If you are flipping a single property, you may consider making it your primary residence until it is sold – this allows you to shift from taxes on the final sale from active income to capital gains which is taxed at a lower price. The key is that for capital gains to apply, the property will need to be in your possession for more than a year, which might not be suitable for every investor’s overall investing plan. This is why it is essential to know which deductions you can make as a non-occupant because living in the property isn’t always an option.

Lastly, you can save by writing off certain expenses that are allowed by the IRS. These deductions include capital expenditures, vehicle expenses, office expenses, building permits, and more. Fix and flip investors can deduct certain expenses before their property is renovated, while some deductions can only be made after the project has been completed and sold successfully.

Tax Example

Let’s set the scene: say that you have purchased a flipping project for the low price of $40,000, of which your total expenses including property renovation come to $38,500 excluding the original purchase price. After successfully marketing the property, you find interested buyers and get a final selling price of $105,000. This would make the total profit of the flip a total of $26,500.

When the time comes for tax to be paid, and if the investor’s ordinary tax rate is 23%, they would owe an income tax total of $6,095 for that financial year. That doesn’t include the self-employment tax that many investors are registered for, coming to 15.3%, which would amount to $4,055.

That would bring the total taxes the investor is liable for in this example to $10,150, leaving them with a profit of $16,350.

Navigating your taxes and staying on top of IRS requirements can be difficult, especially with tax brackets shifting yearly. Many fix and flip investors make use of a tax consultant to confirm that their numbers are accurate and to ensure that they are making use of every deduction they possibly can. That makes keeping detailed records of expenses essential and understanding the basics of how fix and flip taxes are structured will help you make sense of what you are paying and why.

House Flip Details

- Original House Price: $40,000

- Renovations: $38,500

- Resale Price: $105,000

- Total Profit: $26,500

- Property Owner Income Tax Rate: 23%

- Property Owner Self Employment Tax: 15.3%

Final Tax Amount

- Income Tax = $26,500 * 23%

- Income Tax = $6,095

- Self Employment Tax = $26,500 * 15.3%

- Self Employment Tax = $4,055

- Total Tax Payable = $6,095 + $4,055

- Total Tax Payable = $10,150

Final Thoughts

As a real estate investor, once you know how the taxes on flipping houses actually works, the process of filing becomes less daunting. There are many ways to decrease the amount of tax you have to pay legally, from making your investment property your primary home, holding onto it for longer periods of time, registering a house flipping business as an S-corp, and capitalizing on deductions. The profits from property flipping are most commonly treated as ordinary income rather than capital gains, although both can apply depending on how big the taxable amount is and which bracket it falls into.

At the end of the day, don’t let taxes scare you away from flipping houses if you have not done so before – there is still plenty of opportunity to profit.