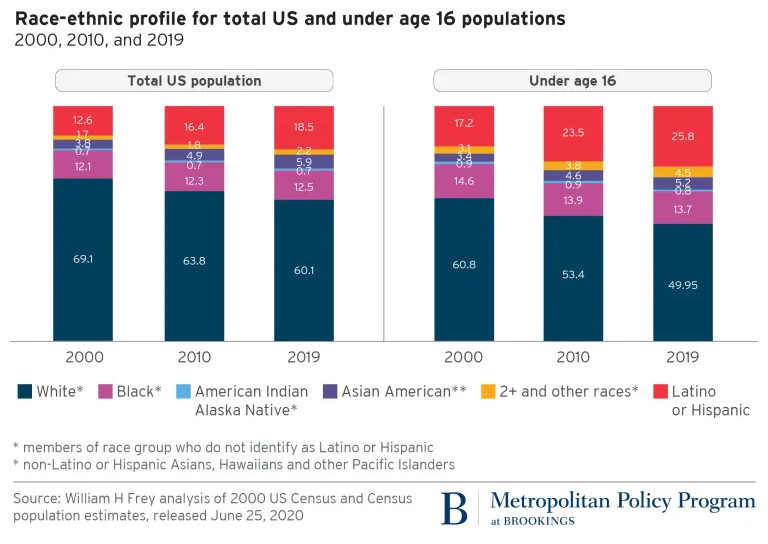

“In 1980, white residents comprised almost 80% of the national population, with Black residents accounting for 11.5%, Latino or Hispanic residents at 6.5%, and Asian Americans at 1.8%. (Except for Latinos or Hispanics, data for all racial groups pertain to non-Latino or Hispanic members of those groups.)

By 2000, the Latino or Hispanic population showed a slightly higher share than the Black population: 12.6% versus 12.1%. The Asian American population share (including Native Hawaiians and Pacific Islanders) grew to 3.8%, while the white population share dropped nearly 10 percentage points, to 69.1%.”

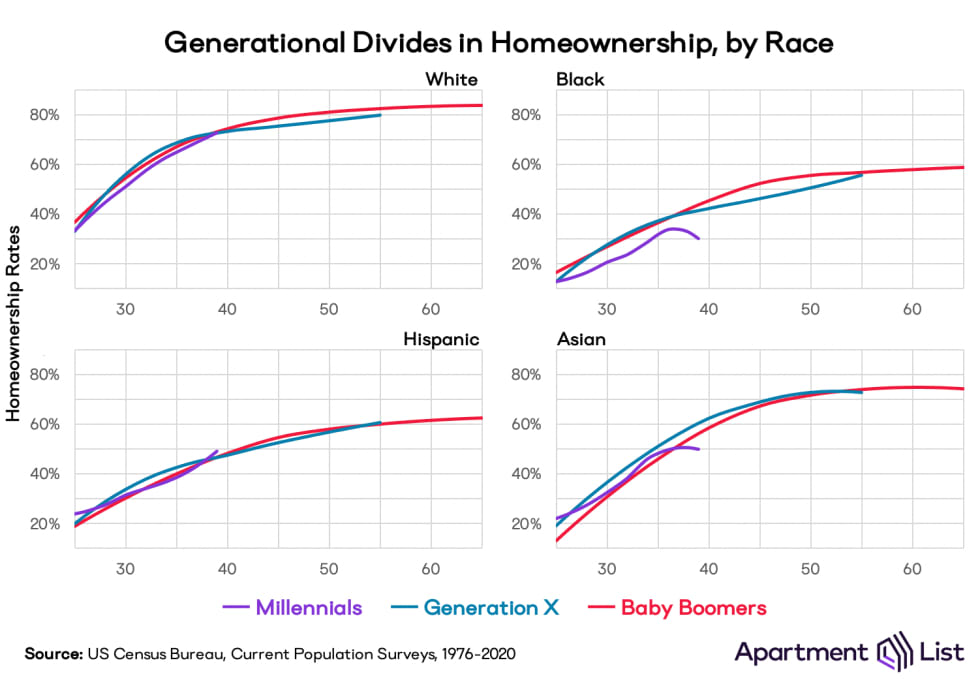

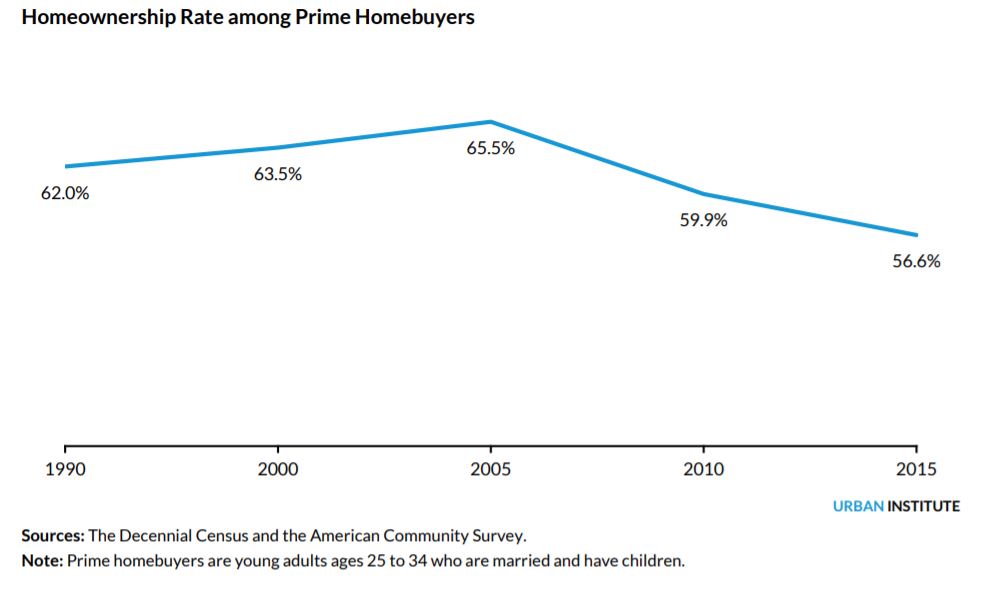

This has a direct bearing on millennial homeownership, because Hispanic, Black, American Indian, and Asian Americans have lower homeownership rates than their White counterparts.

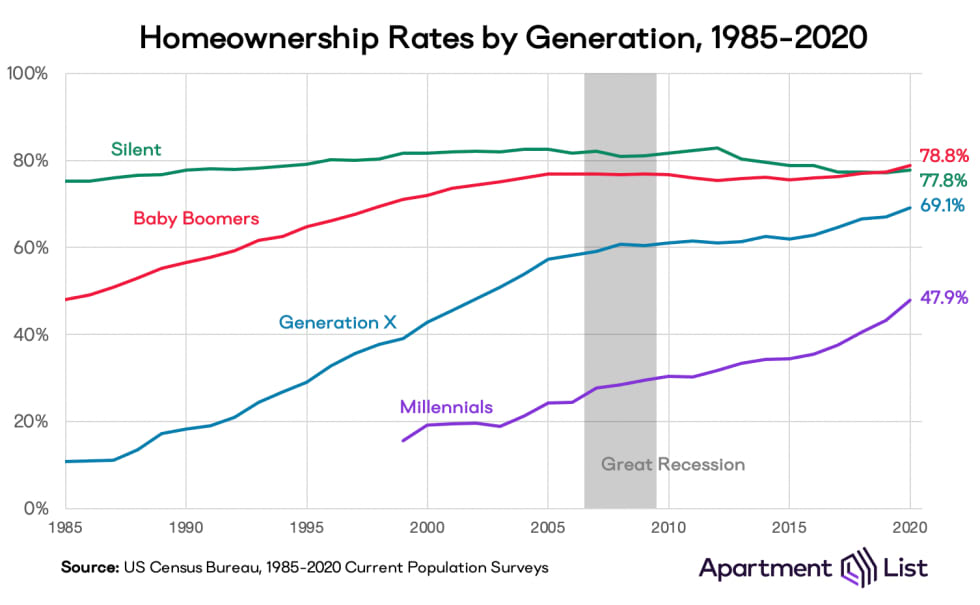

In fact, when you consider this graph published by Apartment List, it’s pretty clear that white millennials are surprisingly close to Generation X and the Baby boomers in terms of homeownership rate.