Hard Money Loans

Data driven hard money lending. Get your loan in under 10 minutes

Best Multifamily Bridge Lenders In 2026

Choosing among multifamily bridge lenders is one of the most important decisions you will make on a transitional deal. The right lender can determine how fast you close, how much leverage you secure, and whether your deal structure truly supports your business plan. From small balance executions to larger institutional transactions, not all lenders operate the same way.

In today’s market, sponsors must weigh speed against pricing, leverage against flexibility, and structure against exit strategy. Some value-add multifamily lenders specialize in heavy rehab and lease-up plays, while others focus on stabilized bridge or bridge-to-agency strategies. Aligning the lender with your deal size and execution timeline can impact returns.

Below, we break down the leading multifamily bridge lenders by tier, compare structures and strengths, and outline how to choose the right partner for your next acquisition or repositioning.

- Multifamily

- Mixed-Use

Lender Comparison Table

| Lender | Min Loan | Max LTV/LTC | Rate Range | Term | Close Time | Recourse | Best For |

|---|---|---|---|---|---|---|---|

| SMALL BALANCE LENDERS | |||||||

| RCN Capital | $250K | Up to 75% LTV (stabilized); 80%+ rehab | Market short-term bridge pricing | 12–18 months | 30–45 days | Recourse typical | Small multifamily bridge, light-to-moderate rehab |

| New Silver | $1M | Up to 85% LTC/LTV | 9.00% – 11.50%, fixed | 12–24 months | 30–45 days | Recourse generally required; non-recourse possible (select CRE) | Small balance value-add, lease-up multifamily (5–65 units, $1M–$5M) |

| Lima One Capital | ~$1M+ | Up to 85% LTC, 70% LTARV | Market bridge pricing (fixed available) | 24–36 months | 30–45 days | Non-recourse available | Value-add, vacancy tolerance, stabilization |

| MID MARKET LENDERS | |||||||

| Ready Capital | $3M | Up to 90% LTV (affordable deals) | Bond/LIHTC-based pricing | 5–17 years | 45–60 days | Recourse through stabilization; non-recourse thereafter | Affordable multifamily, LIHTC, bridge-to-bond |

| Greystone | ~$3M+ | Agency/HUD leverage; program-based | Market agency + floating bridge | Short-term bridge or long-term fixed | 45–60+ days | Frequently non-recourse (agency/HUD) | Mid-market agency, HUD, bridge-to-perm |

| Lument | ~$10M+ | Bridge leverage varies by asset | Floating-rate bridge pricing | 12–36 months | 45–60 days | Often non-recourse (deal-dependent) | Mid-to-institutional transitional multifamily |

| INSTITUTIONAL LENDERS | |||||||

| Walker & Dunlop | ~$1M+ | Conservative bridge; agency-based leverage | Market agency + floating bridge | Short-term bridge or long-term agency | 45–60+ days | Typically non-recourse (agency standard) | Institutional bridge-to-agency, stabilized multifamily |

| Berkadia | Mid-market+ | Agency/HUD leverage | Market agency pricing | Short-, intermediate-, long-term | 45–60+ days | Typically non-recourse (agency) | Agency-backed institutional multifamily |

| ACORE Capital | ~$15M+ | Institutional bridge leverage (deal-specific) | Floating-rate bridge pricing | 12–36 months | 45–60 days | Typically non-recourse | Large value-add, lease-up institutional deals |

| Arbor Realty Trust | ~$8M+ | HUD program dependent (high leverage) | Competitive agency/HUD rates | Long-term; up to 40-year amortization | 60+ days | Typically non-recourse (HUD carve-outs) | Institutional multifamily, affordable, bridge-to-HUD |

Best Multifamily Bridge Lenders by Deal Size

Small Balance Multifamily Lenders (Under $3M)

1. New Silver

| Feature | Details |

|---|---|

| Loan Size | $1M–$5M |

| Rate Range | 9.00%–11.50%, fixed |

| Term & Structure | 12–24 months; interest-only throughout loan term |

| Leverage | Up to 85% LTC/LTV; up to 70% ARV |

| Fees | 1%–2% origination |

| Recourse | Personal guaranty generally required; non-recourse possible on select CRE transactions |

| Best For | Value-add, lease-up, repositioning, light-to-moderate rehab, and heavier redevelopment targeting refinance or sale within 12–24 months (5–65 units) |

New Silver is a direct lender offering a dedicated Multifamily Bridge Program and flexible CRE bridge solutions for transitional assets. The platform focuses on short-term, interest-only financing designed to support value-add strategies with a defined path to refinance or sale.

Pros:

- Competitive commercial short-term bridge pricing

- High leverage up to 85% LTC

- Flexible structuring for multifamily and select CRE assets

- Case-by-case review for larger, complex transactions

Limitations:

- Short-term structure requires a clear exit strategy

- Minimum FICO 660–680; prior track record preferred

- No cash-out refinances under the CRE bridge program

2. Lima One Capital

| Feature | Details |

|---|---|

| Loan Size | Up to $10M+ |

| Rate Range | Market bridge pricing; fixed-rate options available |

| Term & Structure | 24–36 months; interest-only |

| Leverage | Up to 80% LTC/LTV (stabilized); up to 85% LTC / 70% LTARV (value-add) |

| Fees | Market standard origination |

| Recourse | Non-recourse available |

| Best For | Lease-up, repositioning, renovation, or occupancy stabilization prior to agency refinance |

Lima One Capital is a national business-purpose lender providing flexible multifamily bridge financing for value-add and stabilization strategies. The platform is built to help investors move quickly on transitional assets without waiting for agency approval. Low or no in-place DSCR accepted; supports vacant or low-occupancy properties and Freddie/Fannie or bank fallout deals. A delayed acquisition program is available for cash buyers.

Pros:

- High leverage up to 85% LTC

- Flexible DSCR and vacancy tolerance

- Non-recourse options available

- Fixed-rate bridge solutions

- Delayed acquisition program for cash buyers

Limitations:

- Short-term bridge structure requires a defined exit strategy

- Primarily focused on transitional multifamily assets

- Geographic lending restrictions in select states

3. RCN Capital

| Feature | Details |

|---|---|

| Loan Size | $250K–$2M |

| Rate Range | Market short-term bridge pricing |

| Term & Structure | 12–18 months; extended terms available |

| Leverage | Stabilized bridge: up to 75% LTV (purchase), 70% (refi) | Fix & flip: up to 80% of purchase price + 100% of rehab costs; ARV up to 70% |

| Fees | Market standard origination |

| Recourse | Recourse typical |

| Best For | Small to mid-sized multifamily acquisitions or refinances requiring light, moderate, or heavy rehab prior to stabilization or resale |

RCN Capital is a direct lender providing short-term bridge, fix and flip, and long-term rental financing for multifamily properties with 5+ units. The platform is designed for investors executing stabilization, rehab, and repositioning strategies. Minimum 650 FICO required. Mixed-use properties with 70%+ residential use are eligible.

Pros:

- Flexible bridge and fix and flip options

- Up to 100% of rehab costs financed

- Experience-based leverage tiers

- Available for mixed-use properties (70%+ residential)

- Cash-out options available on qualifying deals

Limitations:

- Loan amounts capped at $2M

- Leverage decreases for less experienced sponsors

- Short-term structure requires a defined exit plan

- Heavy rehab restricted for inexperienced borrowers

Hard Money Loans

Data driven hard money lending. Get your loan in under 10 minutes

Mid-Market Multifamily Lenders ($3M–$15M)

1. Greystone

| Feature | Details |

|---|---|

| Loan Size | Mid-market to institutional; recent transactions $30M–$250M+; $12B+ financed in 2024 |

| Rate Range | Fixed-rate agency (Fannie/Freddie/HUD) and floating-rate bridge; market pricing |

| Term & Structure | Long-term fixed for stabilized assets; short-term floating bridge for value-add and lease-up |

| Leverage | Agency/HUD program-based; high leverage available through HUD |

| Fees | Market standard; varies by program |

| Recourse | Typically non-recourse (agency/HUD standard carve-outs) |

| Best For | Multifamily sponsors seeking agency, HUD, or bridge-to-permanent financing with full capital stack access and long-term servicing support |

Greystone is a top-ranked multifamily and healthcare lender with more than 35 years of experience. The firm is a leading HUD lender and a Top 10 Fannie Mae DUS and Freddie Mac Optigo lender, with deep agency relationships and nationwide execution capabilities. Products include CMBS, tax-exempt bonds, mezzanine financing, and debt and equity placement.

Pros:

- #1 HUD multifamily and healthcare lender

- Top 10 Fannie Mae and Freddie Mac lender

- $100+ billion servicing portfolio

- Full capital stack from debt to equity

- Strong track record with institutional-scale transactions

Limitations:

- Institutional underwriting standards

- Agency and HUD timelines can extend closing periods

- Less flexibility for highly distressed or non-conforming assets

2. Ready Capital

| Feature | Details |

|---|---|

| Loan Size | $3M–$100M+ |

| Rate Range | Bond/LIHTC-based pricing; tax-exempt and taxable structures |

| Term & Structure | 5–17 year terms; 40–45 year amortization; interest rate locked 30+ days prior to closing |

| Leverage | Up to 90% LTV; 1.15x minimum DSCR |

| Fees | Market standard; varies by transaction |

| Recourse | Recourse through stabilization; non-recourse thereafter |

| Best For | Affordable multifamily acquisitions, rehabilitation, new construction, or bridge-to-bond LIHTC transactions |

Ready Capital is a national lender focused on affordable housing creation and preservation, with deep experience in LIHTC and bond executions. The firm has facilitated $7 billion in Low-Income Housing Tax Credit financing supporting 75,000 units nationwide. No separate construction lender required; bond structuring and capital stack integration are handled in-house.

Pros:

- Integrated bond structuring with streamlined execution

- High leverage up to 90% LTV

- Interest rate locked 30+ days prior to closing

- No separate construction lender required

- Extensive LIHTC and affordable housing track record

Limitations:

- Focused primarily on affordable and LIHTC transactions

- DSCR and compliance requirements tied to affordable housing guidelines

- Recourse during stabilization period

3. Berkadia

| Feature | Details |

|---|---|

| Loan Size | Mid-market to institutional; $47B in originations across 2023–2024 |

| Rate Range | Market agency pricing (Fannie Mae, Freddie Mac, HUD); structured capital rates vary |

| Term & Structure | Short-, intermediate-, and long-term; fixed and floating options across acquisition, refinance, rehab, and repositioning |

| Leverage | Agency/HUD program-based leverage |

| Fees | Market standard; varies by program and transaction size |

| Recourse | Typically non-recourse (agency standard) |

| Best For | Agency-backed debt, institutional-scale financing, or integrated investment sales and mortgage banking under one platform |

Berkadia is a national leader in multifamily commercial real estate, providing investment sales and mortgage banking solutions across the full capital stack. The firm is ranked #1 Freddie Mac lender (2021–2024) and #2 Fannie Mae DUS lender (2022–2024), with $22B in investment sales and $47B in loan originations across 2023–2024.

Pros:

- #1 Freddie Mac lender (2021–2024)

- #2 Fannie Mae DUS lender (2022–2024)

- $22B investment sales and $47B loan origination volume (2023–2024)

- Full-service platform including sales, debt, and structured capital

- Strong institutional and portfolio execution expertise

Limitations:

- Institutional underwriting standards and documentation requirements

- Agency and HUD timelines may extend closings

- Primarily focused on multifamily and institutional-quality assets

4. Lument

| Feature | Details |

|---|---|

| Loan Size | Typically $10M+; flexible depending on borrower profile and transaction complexity |

| Rate Range | Floating-rate bridge pricing; spreads based on property risk, sponsor experience, and leverage |

| Term & Structure | Short-term, interest-only bridge loans; structured for clear path to permanent debt |

| Leverage | Deal-dependent; varies by asset risk and sponsor profile |

| Fees | Market standard; varies by transaction |

| Recourse | Often non-recourse (deal-dependent) |

| Best For | Value-add or transitional multifamily assets targeting agency or long-term permanent refinance; deals between small balance bridge and institutional agency executions |

Lument is a commercial real estate lender offering a wide range of financing solutions across property types, including multifamily bridge and transitional loans. The platform supports acquisitions, refinances, value-add repositioning, and bridge-to-permanent executions with access to diverse capital sources and balance-sheet execution.

Pros:

- Access to diverse capital sources and balance-sheet execution

- Flexible structuring for transitional and repositioning plays

- Ability to underwrite complex business plans

- Experience with bridge-to-permanent execution

Limitations:

- Typically optimized for mid-market to institutional loan sizes

- Floating-rate bridge structures with interest-only periods

- May require stronger sponsor track records on larger deals

Institutional Multifamily Lenders

1. Arbor Realty Trust Program

| Feature | Details |

|---|---|

| Loan Size | Commonly $8M–$60M+ for FHA executions |

| Rate Range | Competitive HUD-insured rates; program-dependent |

| Term & Structure | Up to 40-year amortization; fully assumable; fixed-rate HUD-insured |

| Leverage | High leverage; HUD program-dependent |

| Fees | Market standard; varies by program |

| Recourse | Typically non-recourse (HUD standard carve-outs) |

| Best For | Multifamily, affordable housing, senior housing, and healthcare investors seeking long-term HUD-insured financing or bridge-to-HUD execution |

Arbor Realty Trust is a nationwide direct lender and REIT specializing in multifamily, senior housing, and healthcare financing. It is a leading Fannie Mae and Freddie Mac lender and an approved FHA MAP and LEAN lender with over 30 years of experience. A dedicated bridge-to-HUD program provides a seamless transition from short-term bridge to long-term FHA financing.

Pros:

- Approved FHA MAP and LEAN lender with nationwide reach

- Strong relationships with HUD offices and third-party vendors

- Bridge-to-HUD program for seamless short-term to long-term transition

- High leverage with long-term amortization and assumability

- Decades of FHA execution experience

Limitations:

- FHA/HUD process is more complex and time-intensive than conventional bridge financing

- Primarily focused on multifamily, senior housing, and healthcare asset classes

2. Walker & Dunlop

| Feature | Details |

|---|---|

| Loan Size | ~$1M+ (small balance) to $100M+ (institutional agency and bridge) |

| Rate Range | Fixed and floating-rate agency pricing; floating-rate bridge at market spreads |

| Term & Structure | Long-term fixed agency with optional interest-only; short-term floating bridge for value-add and lease-up |

| Leverage | Agency-based leverage; bridge leverage may be more conservative than debt funds |

| Fees | Market standard; varies by program and transaction size |

| Recourse | Typically non-recourse (agency standard carve-outs) |

| Best For | Competitive agency financing for stabilized assets or structured bridge capital for transitional multifamily deals targeting agency refinance |

Walker & Dunlop is a top-ranked multifamily lender with access to Fannie Mae, Freddie Mac, FHA/HUD, and an extensive network of capital sources across the U.S. The platform covers the full spectrum of multifamily financing, from small balance agency loans to large institutional bridge executions, with proven bridge-to-permanent execution.

Pros:

- Strong agency and HUD relationships

- Wide capital markets access

- Full spectrum multifamily platform

- Proven bridge-to-permanent execution

Limitations:

- Institutional underwriting standards with detailed documentation requirements

- Agency and HUD processes can involve longer timelines

- Less flexibility on non-conforming assets outside agency or HUD guidelines

- Bridge leverage may be more conservative than some debt funds

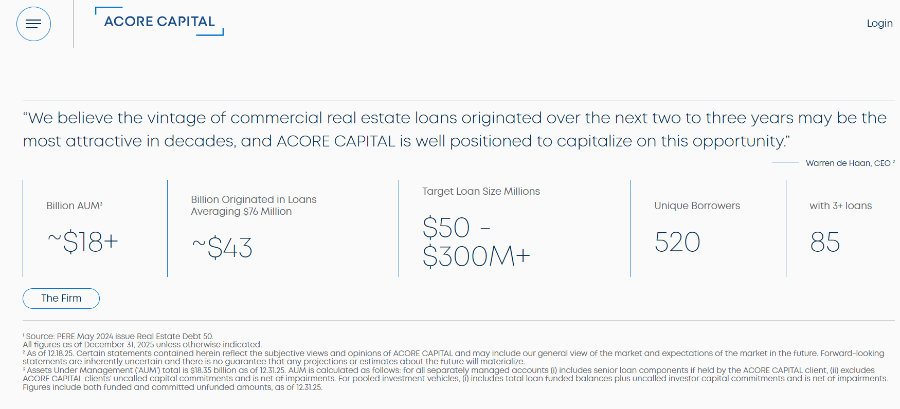

3. ACORE Capital

| Feature | Details |

|---|---|

| Loan Size | Typically $15M+; often significantly larger institutional bridge transactions |

| Rate Range | Floating-rate bridge pricing; spreads based on leverage, asset, and sponsor profile |

| Term & Structure | Short-term, floating-rate, interest-only; senior mortgages and mezzanine/structured capital available |

| Leverage | Institutional bridge leverage; deal-specific |

| Fees | Market standard; varies by transaction size and complexity |

| Recourse | Typically non-recourse |

| Best For | Institutional sponsors executing large value-add, lease-up, or complex transitional deals requiring flexible structuring and certainty of execution |

ACORE Capital is a national commercial real estate debt lender specializing in large transitional bridge financing. The firm provides balance sheet capital for multifamily and other CRE assets, with a focus on value-add, lease-up, and repositioning strategies at institutional scale. Senior mortgages and mezzanine or structured capital solutions are available depending on deal complexity.

Pros:

- Dedicated institutional bridge lender

- Strong execution on large multifamily transactions

- Flexible structuring for transitional and repositioning plays

- Experience with bridge-to-agency exits

Limitations:

- Primarily focused on larger institutional loan sizes

- Floating-rate exposure typical for bridge structures

- Institutional underwriting standards and sponsorship requirements

How to Choose the Right Multifamily Bridge Lender

The multifamily lending landscape is crowded. There are debt fund multifamily lenders, agency-focused bridge lenders, private lenders, and hard money multifamily options. On the surface, many multifamily bridge lenders offer similar terms: short-term financing, interest-only payments, and high leverage. The difference is in execution. Choosing the right lender is about alignment with your deal, your timeline, and your exit strategy.

Look for a Lender That Understands Multifamily

Multifamily lending is different from other commercial asset classes. Lease-up risk, renovation timelines, rent growth assumptions, and refinance projections all require specialized underwriting. Whether you are working with a national platform, a debt fund, or a direct lender offering small balance multifamily bridge loans, make sure they actively finance multifamily properties and understand value-add execution.

Match the Lender to Your Deal Size

Not all multifamily bridge lenders target the same loan sizes. Some debt fund multifamily lenders focus exclusively on institutional transactions above $15 million. Others specialize in small balance multifamily bridge loans between $1 million and $5 million. If your loan request falls outside a lender’s core range, your deal may not receive priority attention or optimal terms.

The same logic applies to asset type. Every lender has specific multifamily bridge loan requirements around leverage, credit, liquidity, and experience. Clarifying those parameters early avoids wasting time.

Evaluate Structure Beyond the Rate

Bridge loan rates for multifamily will vary depending on risk, leverage, and timeline. Lower pricing often comes with more conservative leverage or a longer approval process. Faster closings may come at a premium. When comparing multifamily bridge loans, look beyond the interest rate — consider leverage limits, after-repair value caps, extension options, and exit flexibility. Loan structure often has a greater impact on your returns than a marginal rate difference.

Understand Recourse and Risk Exposure

Structure matters, especially when it comes to liability. Some lenders offer a non-recourse bridge loan from closing, subject to standard carve-outs. Others require recourse through stabilization before converting to non-recourse. Hard money multifamily lenders may require full personal guarantees throughout the term. Your choice should reflect your overall portfolio strategy and risk tolerance.

Prioritize a Clear Exit Strategy

Bridge financing is short-term by design. If your plan is to refinance into Fannie Mae, Freddie Mac, or HUD, the loan must be structured to support that transition. A lender experienced in bridge-to-agency executions will underwrite not just the current numbers but the projected stabilized performance. The right multifamily bridge lenders think about your refinance at closing.

Demand Transparent Underwriting

Multifamily bridge loan requirements should be communicated early — including minimum FICO, experience thresholds, leverage limits, and liquidity expectations. Transparency allows you to evaluate feasibility before investing time and third-party costs. A lender who explains their decision-making process and provides constructive feedback creates a more predictable and collaborative experience.

Consider Execution History

Before selecting among apartment bridge lenders or debt fund multifamily lenders, review their recent transactions and experience with similar strategies. Reliable lenders consistently meet timelines, communicate clearly, and close as structured.

5 Questions to Ask Multifamily Bridge Lenders

- What types of multifamily bridge loans do you finance most frequently?

- What are your typical bridge loan rates for deals like mine?

- What are your multifamily bridge loan requirements for leverage and experience?

- Is the loan recourse or structured as a non-recourse bridge loan?

- How do you structure bridge-to-agency or refinance exits?

Get Started Today

Complete the short form below to speak with a Loan Advisor.

Frequently Asked Questions

The best multifamily bridge lenders depend on your loan size, asset profile, and exit strategy. Institutional sponsors often work with large agency platforms and debt fund multifamily lenders such as Walker & Dunlop, Greystone, Berkadia, and Ready Capital, particularly for larger bridge-to-agency executions.

For small balance multifamily bridge loans, direct lenders like New Silver, Lima One Capital, and RCN Capital are strong options. New Silver, in particular, offers a dedicated Multifamily Bridge Program with competitive fixed rates, high leverage, and flexible structures for value-add and transitional assets. Ultimately, the best bridge lenders are those aligned with your deal size, timeline, and business plan.

Bridge loan rates for multifamily vary based on leverage, sponsor experience, asset condition, and market conditions. In general, multifamily bridge loans today range from approximately 9%–11.50% for value-add and repositioning strategies, with fixed-rate programs available for small balance executions in the $1M–$5M range.

Small balance multifamily bridge loans and hard money multifamily options may price differently than institutional debt fund multifamily lenders. Rate is important, but structure, leverage, fees, and recourse terms should all be evaluated together.

Closing timelines depend on complexity and lender type. Some multifamily bridge lenders can close in 30 days on straightforward transactions. Institutional bridge or HUD-related transactions may take 45–60 days or longer.

Direct lenders focused on multifamily bridge loans, particularly in the small balance space, often move faster due to streamlined underwriting and clearly defined multifamily bridge loan requirements. Preparation, documentation, and sponsor responsiveness also impact speed.

Some multifamily bridge loans are structured as a non-recourse bridge loan, subject to standard bad-boy carve-outs. Others require personal guaranty, especially on higher-leverage or transitional assets.

Debt fund multifamily lenders may offer non-recourse structures more frequently on stabilized deals. Hard money multifamily lenders typically require full recourse. The recourse structure should be clearly defined before closing and aligned with your overall risk strategy.

Yes, but expect more conservative terms. Many multifamily bridge lenders prefer sponsors with prior multifamily or value-add experience. That said, some apartment bridge lenders will consider borrowers transitioning from smaller residential investments into 5+ unit properties, particularly on smaller loan amounts.

Inexperienced sponsors may face stricter multifamily bridge loan requirements, including lower leverage, higher liquidity standards, or stronger credit thresholds. Partnering with an experienced operator can improve approval odds.

Bridge-to-agency financing is a strategy where a short-term multifamily bridge loan is used to acquire, renovate, or stabilize a property before refinancing into permanent agency debt through Fannie Mae, Freddie Mac, or HUD.

The bridge provides time to execute a value-add plan, increase NOI, and meet agency underwriting thresholds. Multifamily bridge lenders experienced in bridge-to-agency transactions structure the initial loan with the refinance in mind, helping reduce exit risk and improve long-term financing outcomes.

Multifamily Loan Resources

A complete guide to multifamily loan types, structures, and what investors need to know before financing a multifamily property.

Learn the key factors that impact multifamily loan interest rates and how to secure the most favorable financing for your investment.

Everything investors need to know about multifamily bridge loans, including structure, leverage, rates, and exit strategies.

How hard money multifamily loans work, when to use them, and what to look for in a lender.