New Silver

Income Fund

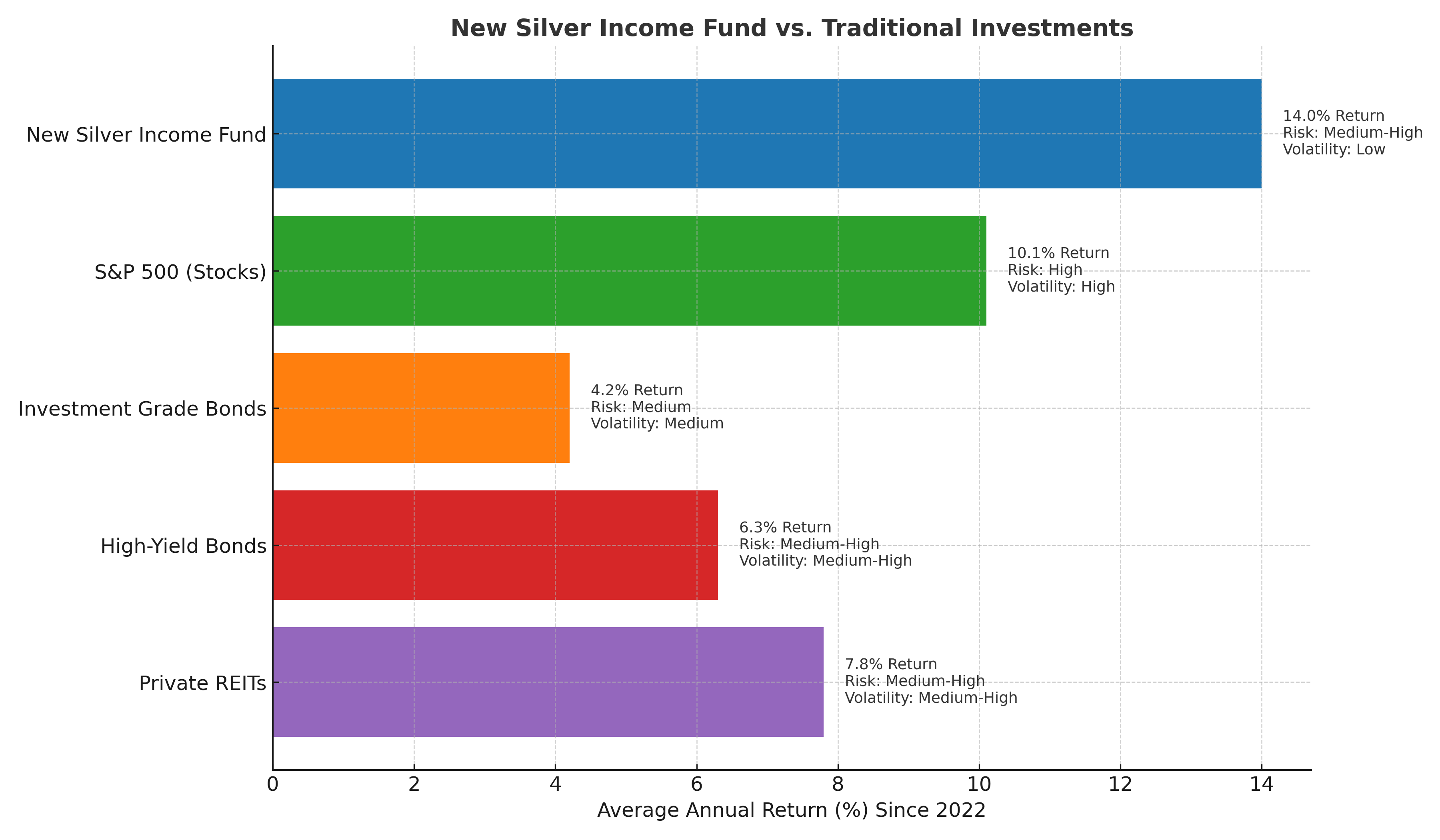

Earn 14-16% Annual Income

- Backed by Residential Transition Loans

- Earn 12% Preferred Return, Paid Monthly

- Plus Annual Profit Sharing Upside

- No Lockup Period

- Quarterly Redemptions Available

- 401K and IRAs Accepted

- Accredited Investors Only

Talk to the Investment Team

Please fill out the below details and a member of our team will contact you within 1 business day.

Investment Overview

The New Silver Income Fund offers accredited investors monthly income by investing in a diversified portfolio of short-term, first-lien residential transition loans (“RTLs”). Backed by a technology-driven platform and institutional underwriting, the Fund targets a mid-teens net annual return through a combination of monthly fixed income and annual profit sharing.

- Monthly Cash Flow: 12% fixed preferred return, paid monthly

- Upside Potential: Annual profit split above 12% — 90% to investors, 10% to manager

- No Lockup: Quarterly redemptions available

- Downside Protection: Loans secured by 1st lien positions and personal guarantees

- Institutional-Grade Infrastructure: Loans held in a bankruptcy-remote indenture trust, providing an additional layer of protection for investors

Key Fund Terms

(paid annually on income above 12%)

1.75% under $150k

1.50% for $150k–$449,999

1.00% for $450k–$999,999

0.75% for $1M+

Accredited investors only

What We Invest In

- Loan Type: Residential Transition Loans

- Avg Loan Duration: 12 months

- Avg Loan Size: $400k

- Use of Proceeds: Fix & flip, ground-up construction, bridge-to-rent

- Loan Security: First-position mortgage and personal guarantees

- Geography: Diversified nationwide portfolio

- Borrower Profile: Experienced real estate investors with equity at risk, high credit score and verified track record

Why Investors Like This Strategy

| Year | Quarter 1 | Quarter 2 | Quarter 3 | Quarter 4 | YTD |

|---|---|---|---|---|---|

| 2025 | 3.49% | 2.32% | |||

| 2024 | 4.03% | 5.09% | 4.33% | 2.45% | 15.51% |

| 2023 | 3.08% | 2.05% | 4.78% | 8.19% | 17.07% |

| 2022 | Inception in May | 3.35% | 4.65% | 3.17% | 14.89%** |

Passive Income Fund Calculator

* Please Note – You can make additional contributions after the initial investment

Income Generation With Residential Real Estate

Residential real estate has been one of the best-performing asset classes over the last few decades, however, most investors don’t have the time to find and diligence the vast opportunities available. Real estate investing typically requires a large amount of capital upfront, the right financial resources, and a high level of expertise. We think there is a better way.

Risk Management

We stress test each loan for profitability, utilize 3rd party independent appraisers and adopt our underwriting to changing market conditions.

- 100% first-lien position on all loans

- Borrower equity required and verified

- Personal guarantees from borrowers

- Construction draws reimbursed only after 3rd-party inspections

- Loans are pledged to trust with oversight by an independent trustee

{kind=link}

Resources

Before investing in New Silver’s Income Fund, make sure that you understand the risks and expenses first. Find out more information about the Fund in our Executive Summary below, and sign up to our monthly newsletter to keep up to date on the Fund’s performance.

Get Started

Schedule a call or contact us directly to learn how the New Silver Income Fund can fit into your income strategy:

This information is intended for accredited investors under Rule 506(c) of Regulation D. Please consult with a financial advisor before making any investment decisions.

Frequently Asked Questions

The Fund targets a mid-teens annual net return, combining the 12% fixed preferred return, paid monthly, with upside through the annual profit split, paid at year-end.

Redemption requests must be submitted via email to [email protected] at least 60 days before the end of a calendar quarter. Proceeds are paid within 90 days after quarter-end, subject to a quarterly limit of 5% of the Fund’s Net Asset Value (NAV). If redemption requests exceed this cap, they are fulfilled pro rata and any remaining balance rolls forward to subsequent quarters.

No. Investors may submit redemption requests quarterly under the terms above.

No. The Fund does not charge redemption fees or impose penalties for exiting the investment.

Management fees are tiered based on your total capital account balance:

- 1.75% annually for investments under $150,000

- 1.50% annually for $150,000–$449,999

- 1.00% annually for $450,000–$999,999

- 0.75% annually for $1,000,000 and above

Your fee tier is based on your aggregate Capital Account balance across all investment accounts associated with you (e.g., individual, joint, and entity accounts). The Manager may combine these for tiering purposes.

No. The 12% preferred return is a fixed target paid monthly from available Distributable Cash. If full payment is not possible in any month, unpaid amounts accrue and must be satisfied before any profit-sharing is paid.

Management fees are paid from income (not investor principal), and any shortfall in the preferred return accrues. Investors are entitled to receive their full 12% preferred return cumulatively before any profit is shared with the Manager.

Redemptions are capped at 5% of total Fund NAV per quarter. If the aggregate investor redemptions request are below the cap, your request will be filled in full. If the aggregate investor redemption requests exceed the cap, you will receive a prorated amount and the remainder will automatically carry forward into the next redemption period.

The annual profit split on earnings above the 12% preferred return is calculated and distributed after year-end financials are finalized and all accrued preferred returns are fully paid.

Any returns above the 12% preferred return are allocated annually — 90% to investors and 10% to the Manager — after all accrued preferred returns are paid.

The Fund accepts capital from individual, joint, entity, trust, and self-directed retirement accounts, including IRA and 401k accounts.

The Fund is structured as a pass-through entity for U.S. tax purposes. Each investor will receive a Schedule K-1 annually. The K-1 reports the investor’s share of the Fund’s income, gains, losses, deductions, and expenses. Taxable income generally includes interest income earned by the Fund from its underlying loan portfolio, and possibly some short-term capital gains. We recommend all investors consult with a tax advisor to understand how this investment fits into their overall tax planning and how income from the Fund may impact their individual situation.

All New Silver loans are secured by a first-lien mortgage on residential investment properties located in the United States. This means the loan holds the senior-most claim on the property in the event of a borrower default. In addition to the mortgage lien, each loan is further secured by personal guarantees from principals of the borrowing entity and borrower equity.

In the event of a borrower default, the New Silver is positioned to take immediate legal and financial action to protect investor capital. Because the New Silver holds a first-lien mortgage on every property, it has the legal right to initiate foreclosure proceedings and recover its investment through the sale of the underlying collateral.

Yes. All investors are provided access to a secure online platform where you can:

- View your account balance and investment history

- Download tax documents and reports

- Monitor distribution activity

- Make additional investment contributions

- Update contact, payment, and account details

The Fund achieves attractive, above-market returns by combining secured lending with the strategic use of senior leverage, without relying on high-risk borrowers or speculative assets. The Fund benefits from a low-cost, secured credit facility to finance a portion of each loan. This allows investors to earn an enhanced return on capital while maintaining disciplined underwriting and downside protection.