Cash-on-Cash Return Calculator

What Is Cash-on-Cash Return?

Cash-on-Cash Return is a simple way to measure how much money you’re making from a real estate investment based on the cash you actually put in. It tells you what percentage of the capital invested you’re getting back each year as profit — in other words, the return on the cash you put into a rental property deal. It focuses only on real, spendable cash, not on the total property value or paper gains.

For example, if you invested $50,000 of your own money into a rental property and it gives you $5,000 in profit after expenses and mortgage payments each year, your cash-on-cash return would be 10%. It’s a quick, easy way to compare different real estate deals or track how well your investment is performing over time.

How Do You Calculate Cash-On-Cash Return?

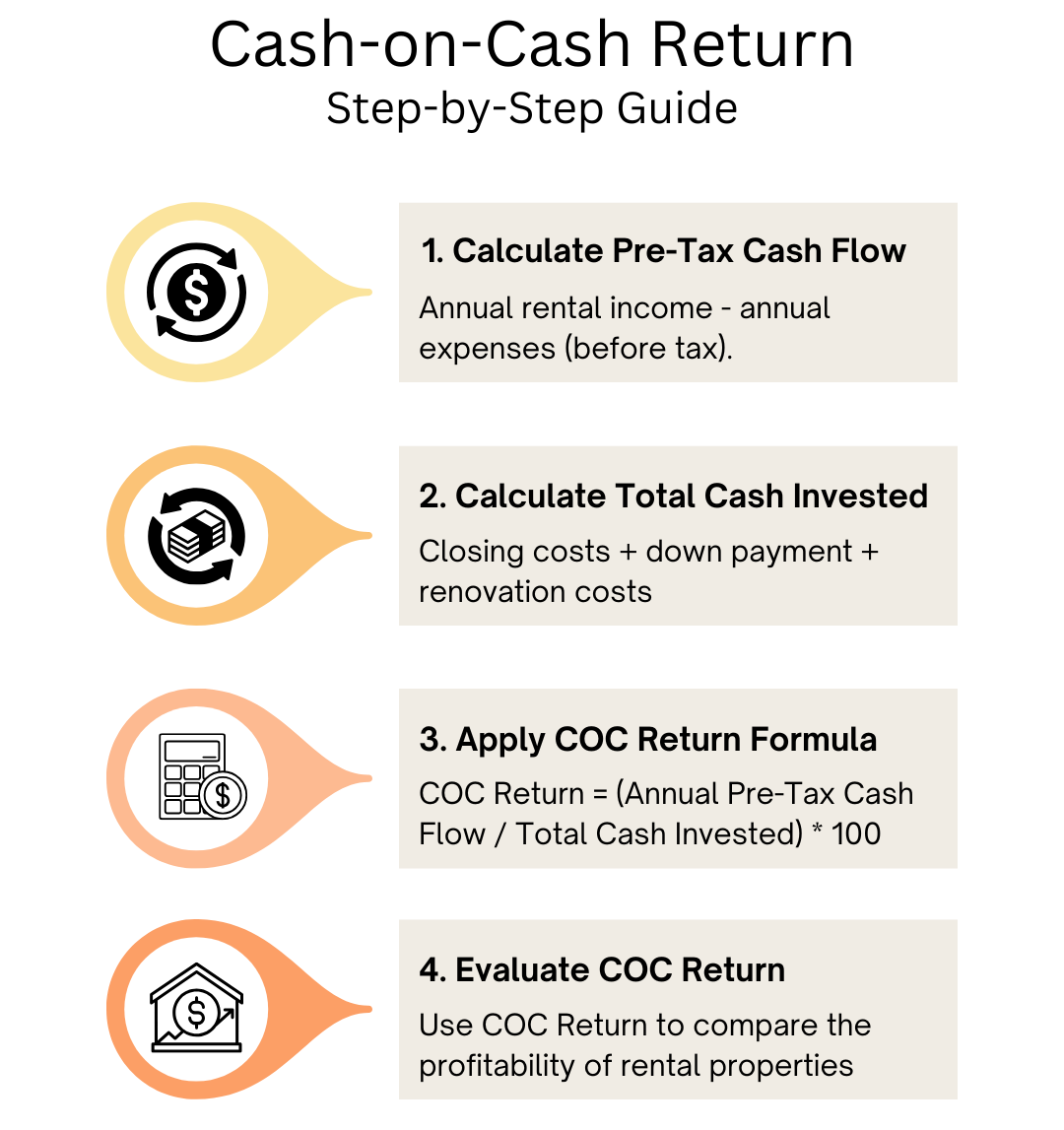

Using the correct mathematical formula is the fastest way to workout the cash-on-cash return.

Cash-on-Cash Return Formula

Cash-on-Cash Return = (Annual Pre-Tax Cash Flow) ÷ (Total Cash Invested) * 100

As you can see, the formula is reasonably straightforward. However, in order to use it correctly, you need to know the Annual Pre-Tax Cash Flow and the Total Cash Invested. Both of these inputs are fully explained below.

Annual Pre-Tax Cash Flow Definition: The cash your property earns you each year after expenses — before taxes

Annual Pre-Tax Cash Flow Formula= (Monthly Rental Income – Monthly Operating Costs – Monthly Loan Payment) × 12

Total Cash Invested Definition: It’s the upfront cash needed to purchase the property — consisting mainly of your down payment, closing costs, and renovations.

Total Cash Invested Formula = Down Payment + Closing Costs + Repairs + Any Other Upfront Costs

Once you have this information, you are essentially just dividing the annual pre-tax cash flow by the total cash invested, and expressing that answer as a percentage.

What You Need To Calculate Cash-on-Cash Return

If you boil it down to the bare essentials, calculating the Cash-on-Cash return of an investment property only require two key pieces of information. How much cash was invested, and the annual pre tax cash flow generated by that investment. However, to get a truly accurate sense of the cash flow that you can expect from a rental property, you need a solid estimate of the rental income, rental expenses, and expected mortgage payments.

Fortunately, New Silver’s Cash-on-Cash Return calculator makes it very easy to workout the expected cash flow. All you have to do is adjust the loan amount, monthly rental income and monthly operating expenses. This information is used to workout the annual pre-tax cash flow.

Once you have the pre-tax cash flow, you literally just need to divide it by the total cash invested and multiply that number by 100 to calculate the cash-on-cash return, expressed as a percentage.

Does Cash-on-Cash Return Include Monthly Loan Repayments?

In short, Yes.

Loan repayments affect the cash flow returns of an investment property, and cash flow is a primary component of the cash-on-cash return formula. So even though loan repayments aren’t directly referenced in the COC Return Formula, they have a fundamental impact on the annual pre-tax cash flow of a property, which has a direct impact on the COC return.

Frequently Asked Questions

Does the Cash-on-Cash Return (CoC) Change Each Year, or Stay the Same?

The annual cash-on-cash return of a rental property can change. It’s not automatically constant.

Cash-on-Cash Return depends on your cash flow, and cash flow can go up or down each year.

Here are the main reasons your cash flow might change, which then affects your CoC return:

1. 📈 Rental Income Can Go Up (or Down)

- If you raise the rent, your income increases.

- More income = more cash flow = higher CoC return.

2. 💸 Expenses Change

Property taxes, repairs, or insurance may go up over time. Or maybe you find ways to cut costs (e.g. self-manage the property).

- If expenses increase, cash flow goes down → CoC return drops

- If expenses decrease, cash flow goes up → CoC return improves

3. 💰 Loan Payments May Stay the Same… or Change

If you have a fixed-rate mortgage, your payment stays the same — so no impact. If you refinance the loan, your payment could change.

- A lower loan payment = higher cash flow = higher CoC return

- A higher loan payment = decreased cash flow = lower CoC return

4. 🧾 One-Time or Ongoing Repairs

You might spend more money in certain years fixing the property.

Additional repairs will reduce your net operating income, cash flow drops for that year → lower return.

Does The Amount Of Cash Invested Ever Change?

Total Cash Invested is typically the constant in the formula. Once you buy the property and make your initial investment — which usually includes:

- Down payment

- Closing costs

- Renovation or repair costs

- Any upfront fees

— that total investment doesn’t usually change. So in most cases, it stays locked in as the denominator in the formula.

However, even total cash invested can change if you invest more money into the property after purchasing it. For instance:

- Major Renovations or Capital Improvements

- You remodel the kitchen or add a new unit.

- Additional Out-of-Pocket Costs

- New roof, HVAC, or foundation work that wasn’t anticipated.

- Cash-in Refinance or Loan Paydown

It is important to note that spending cash on any of the items listed above effectively increases the amount of cash invested in the project.

Does Cash-on-Cash Return factor in home appreciation?

In a word, No. Cash-on-Cash Return does not factor in home appreciation. It only looks at how much actual cash you’re earning each year compared to how much cash you invested. If your property goes up in value, that’s great — but it doesn’t count toward your cash-on-cash return unless you sell or refinance and turn that value into real cash.

In other words, cash-on-cash return focuses only on what’s happening in your bank account right now, not on how much your property is worth on paper.

Additional Resources & Calculators

Workout the potential profitability of an investment property with our Rental Property Calculator.

To figure out the ROI of a fix and flip, you need a comprehensive Hard Money Calculator. It allows you to workout the monthly repayments, analyze net operating income, calculate the return on investment when you sell the property.

Each step in the Buy, Rehab, Rent, Refinance, Repeat (BRRRR) requires detailed analysis before you proceed with the deal. Fortunately our BRRRR Calculator breaks the process down into simple phases that are pretty easy to understand.

Quickly assess the After-Repair Value of a property with our user friendly ARV Calculator.

Cap Rate is a simple formula that helps investors work out how profitable an investment property is likely to be. Our Capitalization Rate Calculator makes this easy to do, in very little time.

FlipScout is a free search engine for property flippers. It lets you find properties that you can earn the highest return on when completing a fix and flip or fix-to-rent project. You can learn more about FlipScout here.

Quickly estimate the ROI of each home renovation project that you execute when flipping or renting investment properties.

Workout the net profit, ROI, maximum loan amount and monthly payment when building properties from the ground up. Ideal for estimating the profitability of a project.

Workout the annual depreciation for each and every year of an investment property's useful life. Made for residential and commercial properties.

This passive income calculator can help you understand how much you need to save each month to generate long term passive income.

Quickly estimate the ROI of each home renovation project that you execute when flipping or renting investment properties.

This calculator can help you decide if you should rent a property, or sell it and reinvest the profits. It provides a detailed analysis of each scenario, and it is very easy to use.